Consumers keep heading to dealers despite rising interest rates contributing to prices at or near all-time highs as new vehicle sales are expected to rise by double digits compared to July 2022.

S&P Global predicts July sales will come in 18% higher than last July’s numbers, but the critical point is what’s driving the push to buy cars, trucks and utility vehicles in the U.S. Actually, the numbers are up because fleet and retail sales are on the go.

“New light vehicle sales will continue to progress in July, reflecting the current trend of sustained demand levels to the fleet sector while retail sales continue to climb,” said Chris Hopson, principal analyst at S&P Global Mobility.

“From both an economic growth and auto demand perspective, the first half of 2023 has proven once again that one shouldn’t doubt the spending capacity of U.S. consumers.”

Tracking the numbers

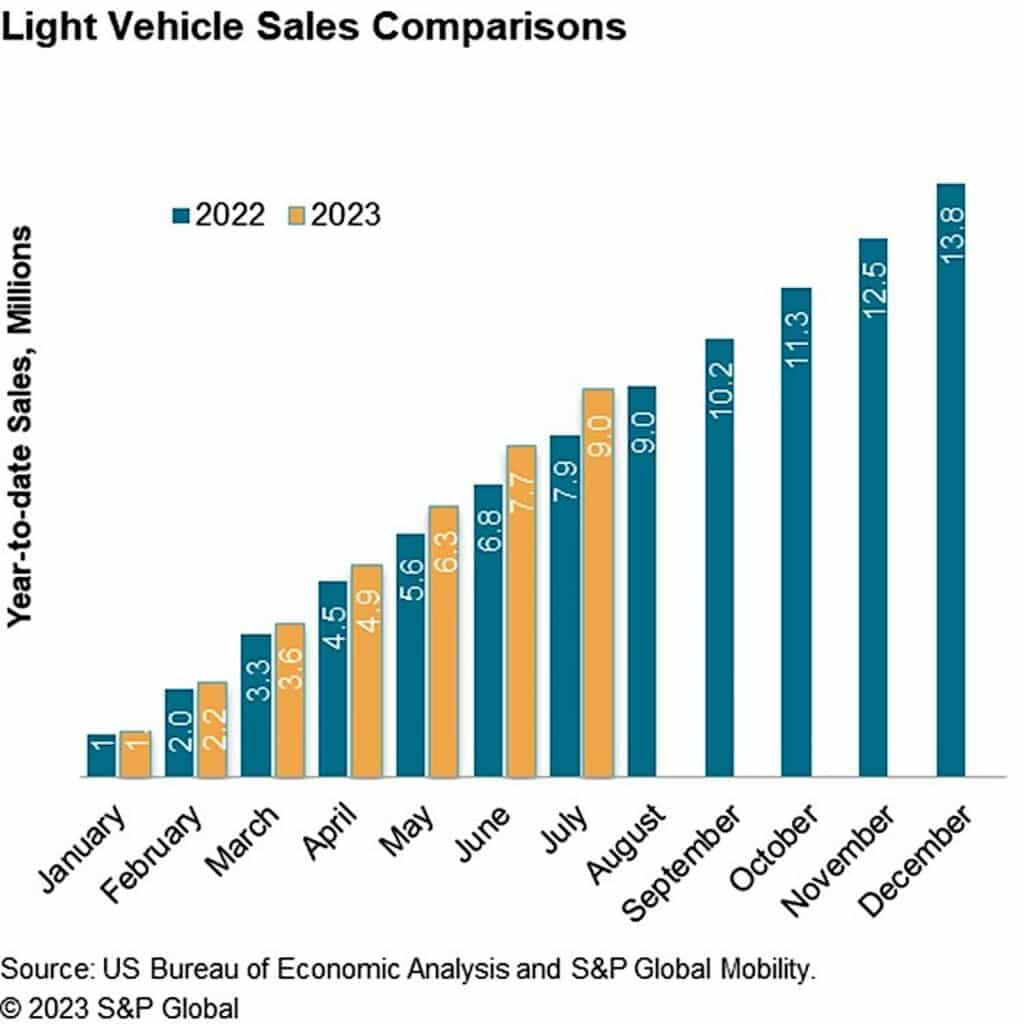

S&P projects new U.S. light vehicle sales volume in July 2023 to reach 1.33 million units.

The expected monthly results represent a full calendar year worth of consecutive monthly sales growth (as measured in year-over-year unadjusted monthly volume comparisons), reflecting the recovery from the depths of the supply chain constraints realized through much of 2022.

This volume would translate to a seasonally adjusted annual rate of 16.1 million units, the company noted.

The first six months of 2023 have outperformed S&P Global Mobility’s estimated, and as a result, S&P Global upgraded its calendar year 2023 U.S. light vehicle sales forecast to 15.4 million units (up from 15.1 million in its previous forecast release).

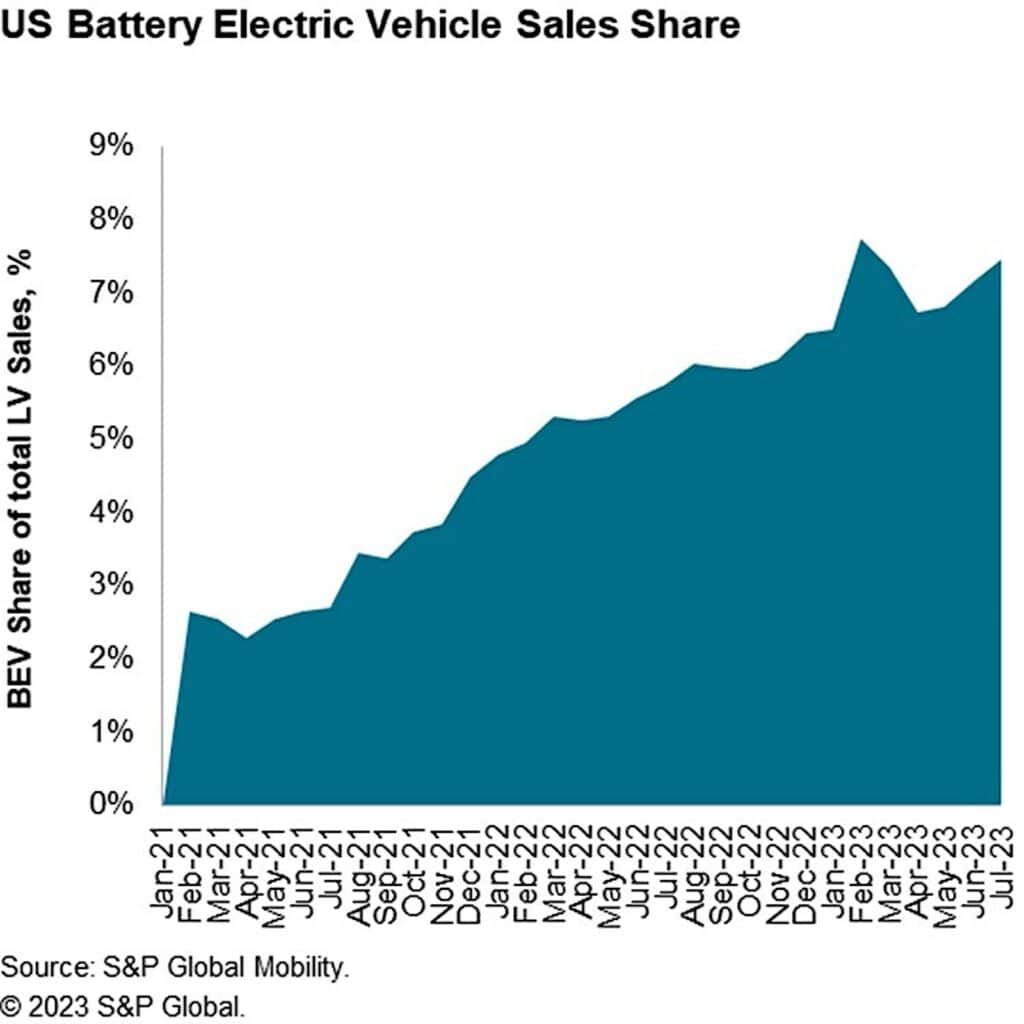

Battery electric vehicle (BEV) remain strong with the vehicles is expected to account for 7.6% of July sales. Continued development of BEV sales remains a constant assumption for 2023 although some month-to-month volatility is expected as BEV pricing changes remain dynamic especially as aggressive BEV production expectations and new product introductions gain momentum in the second half of the year.

Second half swoon?

Many analysts and automakers have predicted sales will slow in the second half of 2023. All have cited affordability issues, including a tighter credit market and it’s being reported the Fed is looking at raising interest rates again, after taking a break at the last chance.

However, S&P isn’t entirely convinced bad news looms on the horizon as efforts by automakers to sort out sort out the troublesome issues plaguing the supply chain appear to be resolved — at least for the moment — allowing them to rebuild their inventories.

Although the July 4 weekend represented a trifecta of the end of the month, end of the quarter, and a holiday weekend, the sales pattern for the weekend was consistent to preceding months-end in terms of sold inventory, the company noted.

“The long weekend took a chunk out of available advertised inventories – from 1.843 million in mid-June to 1.761 million on July 3,” said Matt Trommer, associate director of Market Reporting at S&P Global Mobility. “Perhaps more notable is that available inventories in mid-July almost immediately rebounded to 1.867 million, surpassing the year-to-date highs seen in mid-June.”