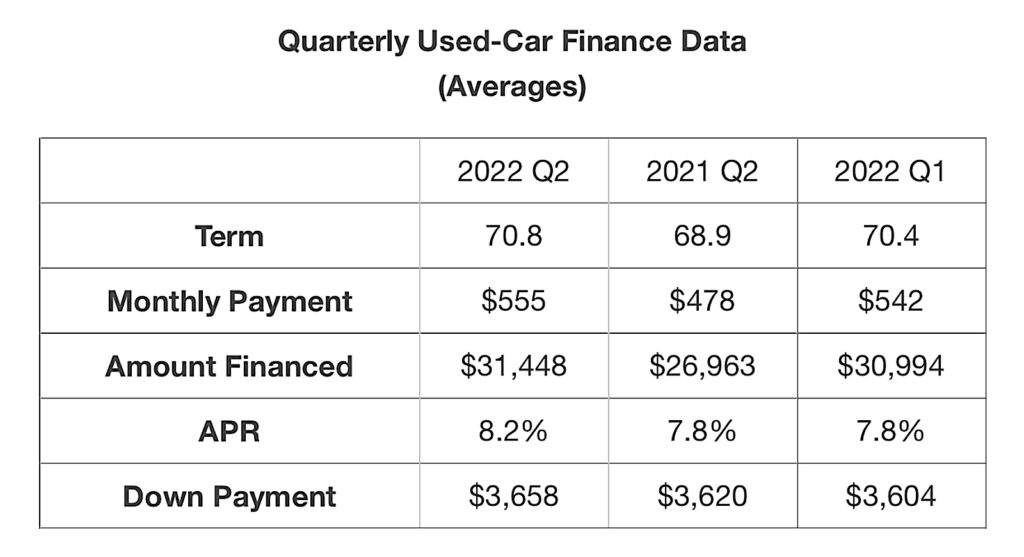

Seemingly each month brings consumers face-to-face with the prospect of paying more than ever for a new vehicle. The monthly new car payment not long ago was a little more than $550 a month, now the average used car payment is higher than that.

Recently, according to Cox Automotive, the average monthly payment for a new vehicle surpassed $700. However, with the Federal Reserve’s rate hike June 15, financing a new car, truck or SUV for that also near record price exceeding $47,000 on average just became more expensive.

No statistic reflects that better than the fact that 12.7% of new vehicle buyers who financed their purchase are now paying more than $1,000 a month for that new vehicle. By comparison, the average rent payment in the U.S. right now is $1,326 a month while the average mortgage payment is $2,064 on 30-year fixed mortgage.

Why so much?

Some folks are paying nearly as much for what they drive as where they live. Part of that is due to rising prices that have consistently set new highs month after month for the past 18 months. But also, folks are financing larger amounts to get those vehicles.

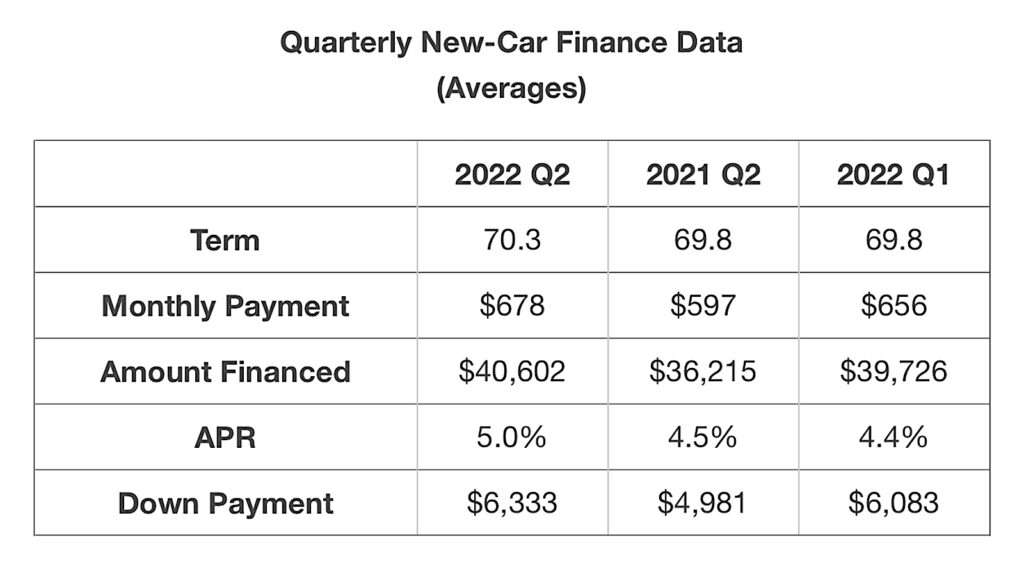

The average amount financed for new vehicles hit a near-record level in the second quarter of 2022, climbing to $40,602 — compared to $39,726 in Q1 2022 and $36,215 in Q2 2021, according to analysts at online shopping guide Edmunds.

The analysts note that the first and only other time that the average amount financed for new vehicles surpassed $40,000 was Q4 2021, when the average annual percentage rate (APR) was just 4.1 percent. Now the average APR is 5%, a significant jump and bump in monthly payment.

Four-digit monthly note

The jump is likely, in some cases, for those monthly car payments looking more like rent payments. The number of consumers sporting a $1K monthly new vehicle payment has skyrocketed, accounting for just 7.3% of buyers in June 2021, 4.6% in June 2019 and a mere 2.1% in 2010, Edmunds noted.

“Low interest rates used to be one of few reprieves for car shoppers amid elevated prices and supply shortages. But the Fed rate hikes this year are making finance incentives far costlier for automakers, and consumers are starting to feel the pinch,” said Jessica Caldwell, Edmunds’ executive director of insights.

“Although there appears to be a steady stream of affluent consumers willing to commit to car payments that look more like mortgage payments, for most consumers the new car market is growing increasingly out of reach.”

Other market drivers

Another reason for the leap in the average price and payment is the rise of electric vehicle sales. Yes, they are good for the planet and fun to drive, but that comes at a cost — a literal one. The average mainstream vehicle costs about $43,000 while the average EV exceeds $61,000.

In recent months, several auto executives, including CEOs, have been sounding the alarm about the fact that EVs are driving up prices and unless something changes, all of the promise EVs will be lost because no one can afford them.

Stellantis CMO Arnaud Deboeuf was the latest executive to ring the bell, warning of a complete “collapse” if BEVs are priced out of reach of the typical motorist. Last December, Toyota CEO Akio Toyoda sounded a similarly apocalyptic note in his role as the chairman of the Japan Automobile Manufacturers Association, or JAMA. Ford CEO Jim Farley and Deboeuf’s boss, CEO Carlos Tavares, issued similar messages recently.

But Stellantis CMO Debouef’s warning comes at a time when the industry is facing severe shortages of key EV components, such as semiconductor chips, that have begun driving up costs. And even if consumers accept the need to switch from gas and diesel to electric vehicles, “the market will collapse” if the industry can’t bring prices under control, he warned. “It’s a big challenge,” he said, according to Bloomberg news.

They are !@#$% nuts to have a car payment that high. If and when the manmade chip shortage is settled, prices will fall and they will be upsidedown with their vehicles worth vs what they owe.