U.S. new car sales are now running at an even lower rate than were seen during the depths of the Great Recession – though there is a small silver lining, as the downturn this month isn’t quite as bad as many analysts had been forecasting.

With automakers and dealers looking for ways to prop up demand any way possible – including online sales and record incentives – the industry has showing “surprising strengths” said Tyson Jominy, a senior executive with J.D. Power, during a Wednesday afternoon webinar.

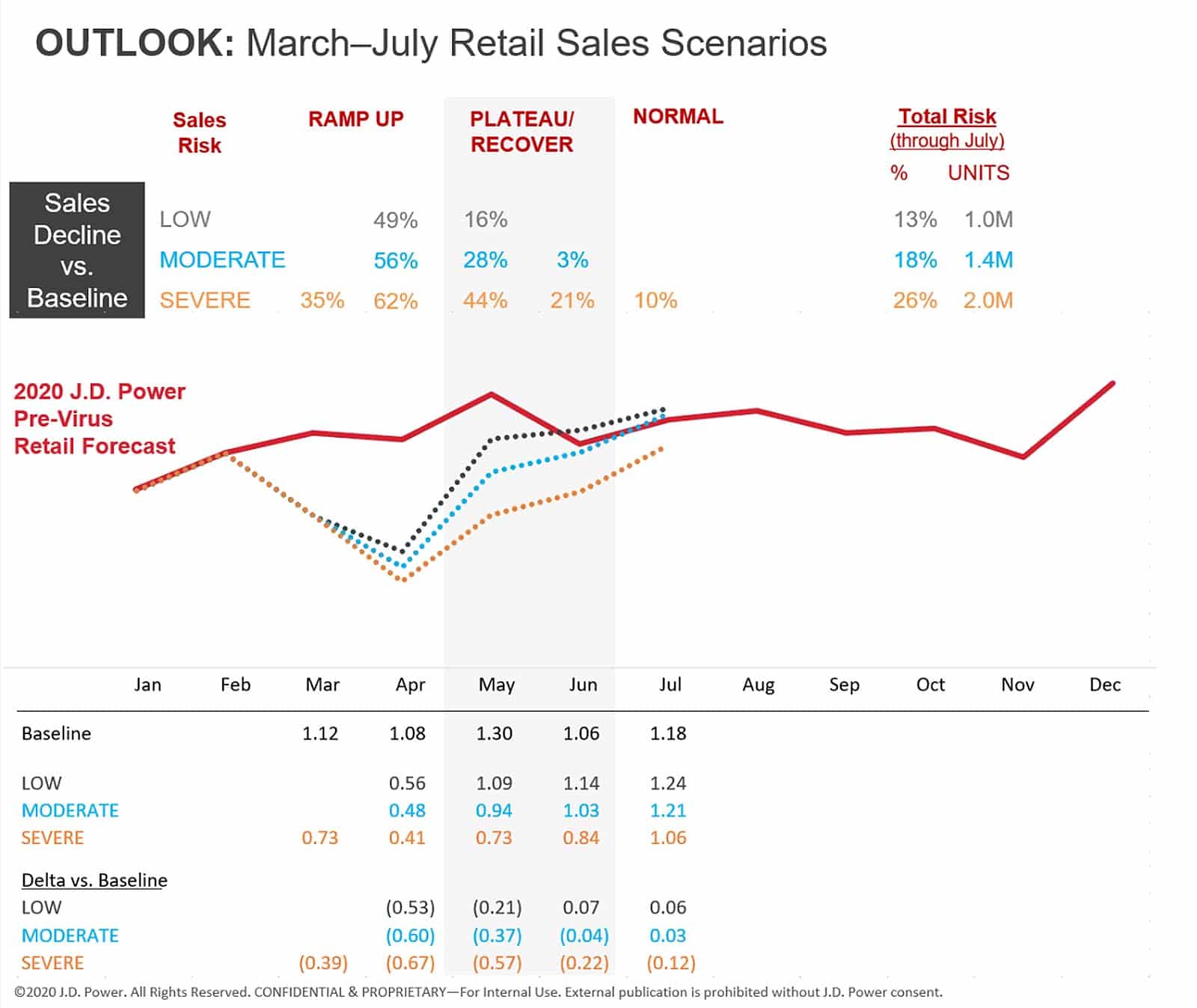

“Things have flattened out,” said Jominy, with demand during the first two weeks of April down about 55% compared to year-ago levels. While that might seem a pretty awful number, Power analysts had originally expected to see new vehicles sales this month fall a whopping 80% after the 39% slide in March due to the coronavirus pandemic.

(Auto sales continue tumbling, but not as badly as expected.)

With all but a handful of states now enforcing shelter-in-place orders, it would seem obvious that the market would be in trouble. Add the fact that three states have completely banned sales, while 24 others – collectively representing about half of the U.S. market – have severely restricted retailers, in some cases allowing them to operate only online.

Some of the country’s biggest markets have effectively dried up entirely, demand just above zero in Detroit and not much higher in New York, noted Jominy, the head of Power’s PIN network which tracks U.S. sales by directly accessing thousands of dealer’s computers in real time. San Francisco experienced a modest uptick during the week ending April 12, Jominy noted, but was still off 70% year-over-year.

A handful of markets, such as Dallas and Phoenix are a bit closer to normal. In many cases that reflects their focus on pickups which are now carrying all-time-high incentives of more than $7,000 apiece.

Automakers have been tinkering with deals, looking for the most appealing formula, and have found some success with stretched-out loans offering zero-interest financing, as well as packages that cover buyers in the event they lose their jobs. That sort of assurance program can play well at a time when nearly 20 million Americans have been sent to the unemployment lines over the past three weeks.

Ironically, while sales are down, transaction prices are running at or near record levels of around $35,600, noted Tom King, Power’s chief data officer. That reflects the way 84-month loans with zero-interest financing can let them buy “more vehicle” for less of a monthly payment said King.

As was the case in recent weeks, the luxury market has been particularly hard hit by the pandemic. That reflects the fact that the majority of high-end buyers lease their vehicles – and lenders are letting them hang onto their vehicles even beyond the official end of their contracts.

(Pandemic will have “a permanent effect” on auto industry.)

On the plus side, said King, “These customers are poised to drive a recovery” when the economy starts returning to normal because there will be so many more lessees needing to get new vehicles at the same time.

How soon the recovery will occur and how high the market will rebound remains uncertain,

Jominy and King agreed. It does not look like any significant uptick in sales will occur before July, and that timetable could stretch out should shelter-in-place plans be extended,

For the moment, Power analysts are expecting 2020 will see new vehicle sales slide to somewhere between 12.4 million and 14.1 million. Their original, pre-pandemic estimate was in the 16.5 million range, down from 17.1 million in 2019.

The slightly better-than-expected April sales could provide a bit of a “tailwind,” said King, but he cautioned that “We have real economic damage occurring every day,” which likely means any significant revival of the American auto market won’t happen before 2021.

Most industry analysts expect that automakers will wait to get a sense that the market is beginning to bounce back and then launch even heftier incentives than are now available. On average, givebacks averaged around $4,100 for all vehicles at the beginning of this year but could surge as high as $5,700 by the end of 2020, said King.

(Car dealers struggling to cope with coronavirus turn to online, “touchless” car sales.)

That might help rebuild demand, he said, but the industry “could wind up in a situation where the average vehicle in the U.S. would be sold at a loss, which is not sustainable.”